How accredited investors are finding yield and stability in a non-market-correlated asset class

Most people don’t realize that life insurance — the same financial product designed to protect families — also holds one of the most overlooked investment opportunities in the private markets.

Each year, Americans allow more than $200 billion in life insurance to lapse or be surrendered for pennies on the dollar. Policies people spent decades paying into are quietly discarded, giving insurance carriers a financial windfall.

But there is a different path — one that transforms forgotten insurance contracts into a stable, actuarially grounded income strategy for accredited investors.

It’s called the life settlement market, and it’s rapidly gaining attention from family offices, wealth advisors, and sophisticated private investors seeking predictable income, portfolio diversification, and insulation from market volatility.

What Is a Life Settlement?

A life settlement occurs when a policyholder sells their life insurance policy to a licensed provider for a lump-sum cash payment that exceeds the insurance company’s surrender value.

The investor (or investment entity) then:

becomes the beneficiary

continues premium payments

receives the full policy benefit at maturity

It is contractual, regulated, and independent of stock market swings — driven instead by actuarial science and demographic trends.

Why Investors Are Paying Attention

The investment world is changing. Rising rates, equity volatility, and slower real-estate cycles have pushed investors to look beyond traditional holdings.

✅ Non-Market-Correlated Cash Flow

Life settlements are tied to life expectancy, not economic cycles. They don’t move with stocks, property values, interest rates, or inflation headlines.

This makes life settlements a stabilizing anchor in modern portfolios.

According to the 2023 Allianz Global Investor Survey,

73% of affluent investors are increasing allocations to private alternatives to offset market volatility.

✅ Attractive Risk-Adjusted Returns

Industry research shows historically 7%–14% annualized returns depending on portfolio construction and underwriting quality

(Conning Research: Life Settlements Report, 2023)

Returns are driven by contractual policy payouts — not speculation, leverage, tenants, or market sentiment.

✅ Massive Supply Opportunity

More than 90% of life insurance policies never pay out, meaning policyholders either surrender them or let them lapse.

That creates a deep pipeline of policy supply and a repeatable opportunity set for investors.

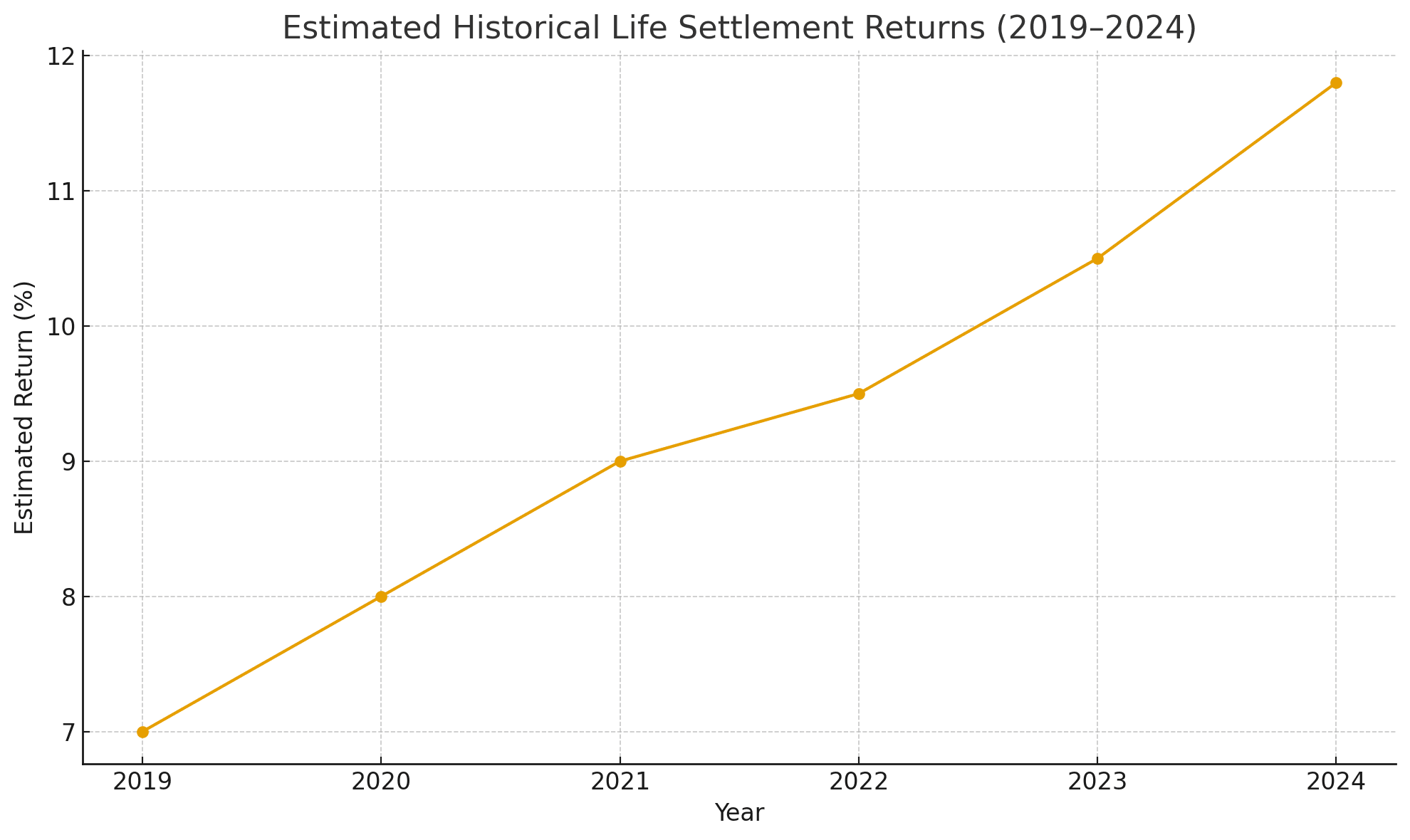

Historical Performance Snapshot

Life settlement performance has demonstrated consistent growth in recent years:

This steady trajectory supports why allocators increasingly view life settlements as a defensive-income asset — especially during uncertain markets.

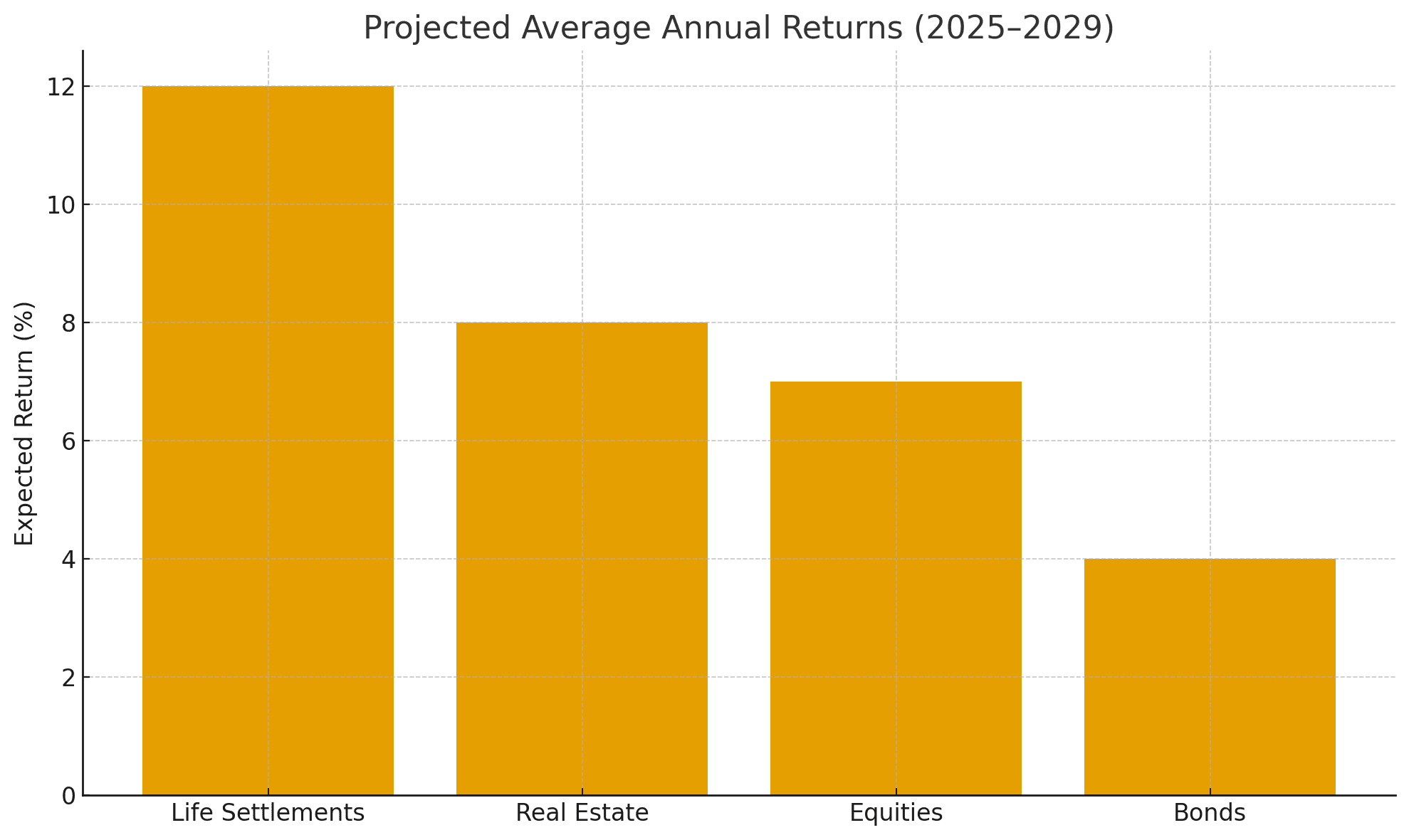

Projected Return Comparison

When looking at the next five years, life settlements are positioned among the strongest passive return drivers:

While equities and real estate remain core holdings, life settlements are emerging as a high-yield, low-volatility complement for sophisticated portfolios.

A Simple Example

A retired policyholder owns a $1 million life insurance policy they no longer need. Without a life settlement, they might surrender it for a minimal amount — or let it lapse entirely.

Through a life settlement, they instead receive a meaningful cash payout today.

An investor acquires the policy, services the premiums, and ultimately receives the contractual $1 million benefit at maturity.

There are:

no market timing decisions

no tenant risk

no earnings reports

no economic cycles to predict

Just actuarial math, regulatory oversight, and contractual value.

Investors may purchase a single policy or participate in professionally constructed, diversified portfolios for broader risk distribution.

Why This Strategy Is Resonating Now

Accredited investors today want:

Reliable passive income

Low-volatility alternatives

Assets not tied to the Fed or public markets

Institutional-level underwriting and transparency

Life settlements offer exactly that — backed by decades of insurance-sector regulation and actuarial rigor.

Who Is This Designed For?

This strategy attracts:

Accredited Individuals

Family Offices

Wealth Advisors & RIAs

High-net-worth retirees reallocating capital

Private market allocators seeking stability

Many investors see life settlements as a way to balance equity exposure, hedge real-estate cycles, and improve long-term cash flow reliability.

The Bottom Line

Life settlements are no longer a niche strategy — they’re a credible income solution in the private markets.

In an era of uncertainty, investors increasingly value assets where the outcome is contractual, not theoretical.

Life settlements fit that definition.

When most people walk away from life insurance value, informed investors step in — and build long-term, disciplined, patient income from a previously untapped source.

Sometimes the smartest opportunities are hiding in plain sight — inside an asset the world forgets.

To learn more about life settlement investments or request our free Abbistar Investor & Policyholder Guide:

📞 877-222-4782

🌐 investabbistar.com

📩 ariel@abbistar.com

investabbistar.com/blog/unlocking-income-from-unused-life-insurance-policies

https://calendly.com/ariel-abbistar/30min